LAST WILL & TESTAMENT

“Every soul shall taste death”

Qur’an, Surah Al-Imran (3:185)

The importance of the Islamic Will (Wasiyya) is clear from the following two hadith:

“It is the duty of a Muslim who has anything to bequest not to let two nights pass without writing a Will about it.”

(Sahih al-Bukhari)

“A man may do good deeds for seventy years but if he acts unjustly when he leaves his last testament, the Wickedness of his deed will be sealed upon him, and he will enter the fire. If, (on the other hand), a man Acts wickedly for seventy years but is just in his last Will and Testament, the goodness of his deed will be Sealed upon him, and he will enter the garden.”

(Ahmad and Ibn Majah)

The Will gives the Testator an opportunity to help someone (e.g. a relative need such as an orphaned grandchild or a christian widow) who is not entitled to inherit from him.

The Will can be used to clarify the nature of joint accounts, those living in commensality, appointment of Guardian for one’s children and so on. In countries where the intestate succession law is different from Islamic law it becomes absolutely necessary to write a Will.

WHY PLAN FOR RETIREMENT?

Retirement planning is key if you want to maintain your lifestyle at retirement. Planning consists of two phases:

Pre-retirement funding which means investing in a Retirement Annuity while you are actively working. Things to consider include how much you can currently afford to invest and how long you have until you reach retirement age.

Post-retirement income requires investing the proceeds of your Retirement Annuity into a Life or Living Annuity. Post-retirement income considerations include choosing a product that is able to sustain capital growth. You can opt to receive income monthly, bi-annually or annually.

FEATURES AND BENEFITS OF A RETIREMENT ANNUITY

- You can invest in Unit Trusts of your choice to save for your retirement

- Minimum contribution of R500.00 per month or R20 000.00 lump sum

- Contributions to a Retirement Annuity are Tax Deductible

- Restrictions ensure your money is kept for your retirement

- Your money is protected from Creditors

- Save on Estate Duties

- A great way to save if you don’t have a company pension fund

BENEFITS OF TAKING A RETIREMENT ANNUITY AT ANGLOWEALTH

- Superior long-term growth with low fees

- We are affiliated with various top tier companies, allowing us to offer a bouquet of retirement products from the various funds

- Clear and transparent reporting

“Investing today buys you days so you don’t have to work tomorrow”

PERSONS FOR WHOM A RETIREMENT ANNUITY IS SUITED

- Persons who are self-employed and not a member of a pension or provident fund;

- If your employer is not contributing to a pension or provident fund on your behalf;

- Where a variable income is taken into consideration when calculating your contribution to a provident or pension fund;

- When you want to supplement your existing retirement savings.

WHEN CAN YOU HAVE ACCESS TO YOUR RETIREMENT ANNUITY FUNDS?

- You can only access your money after the age of 55

- If you become permanently disabled

- If you emigrate

- If your investment is below the minimum requirements applicable at the time

- Death prior to retirement. An RA does not form part of your estate so it will not attract estate duty.

LIMITATIONS ASSOCIATED WITH A RETIREMENT ANNUITY

- You can only access your funds after the age of 55 (except in *certain circumstances listed above);

- Upon retirement, you can only withdraw one third as cash;

- The rest must be invested to provide you with retirement income;

- Prescribed legal investments are limits which restrict amounts you can invest in high-risk investments.

Endowment

WHAT IS AN ENDOWMENT PLAN?

An Endowment is a focused investment which is the perfect vehicle for your goal-orientated savings. Whether it's saving for that new car, your children’s education or that Hajj trip you’ve always dreamed about.

The cost effectiveness of endowments benefit investors with a marginal tax rate 30% and a minimum investment horizon of 5 years.

The underlying investment options are from the range of top-performing Shariah compliant Unit Trusts which have consistently delivered strong investment returns since inception. The consistency of the investment performance is reflected in these funds being awarded numerous local and international investment performance accolades.

ENDOWMENT FEATURES

- Fixed Investment Period;

- Minimum term is 5 years;

- One withdrawal permitted during the 5 year terms;

- You have a choice of the underlying portfolios, allowing you to choose Shariah-Compliant funds.

“Do not save what is left after spending, but spend what is left after saving” – Warren Buffet

UNIT TRUST VS ENDOWMENT

| UNIT TRUST | ENDOWMENT |

| Taxed at your marginal rate, up to 41% | Taxed at 30% |

| May use your interest exemption | No interest exemption |

| May use your capital gains exemption | No capital gains exemption |

| Flexible and accessible | Minimum 5 year term |

| No option to cede as security | May cede as security |

| No option to appoint beneficiary | May appoint beneficiary |

| Tax efficient for individuals with a marginal tax rate below 31% | Tax efficient for high-income earners who have used up their interest exemption |

BENEFITS

- Estate planning benefits;

- Taxed within the investment at 30%;

- Beneficiaries have access to your investment in the event of your death;

- Minimum contribution: R500.00 monthly or R20 000 lump sum;

- Investment can be ceded as security for a loan.

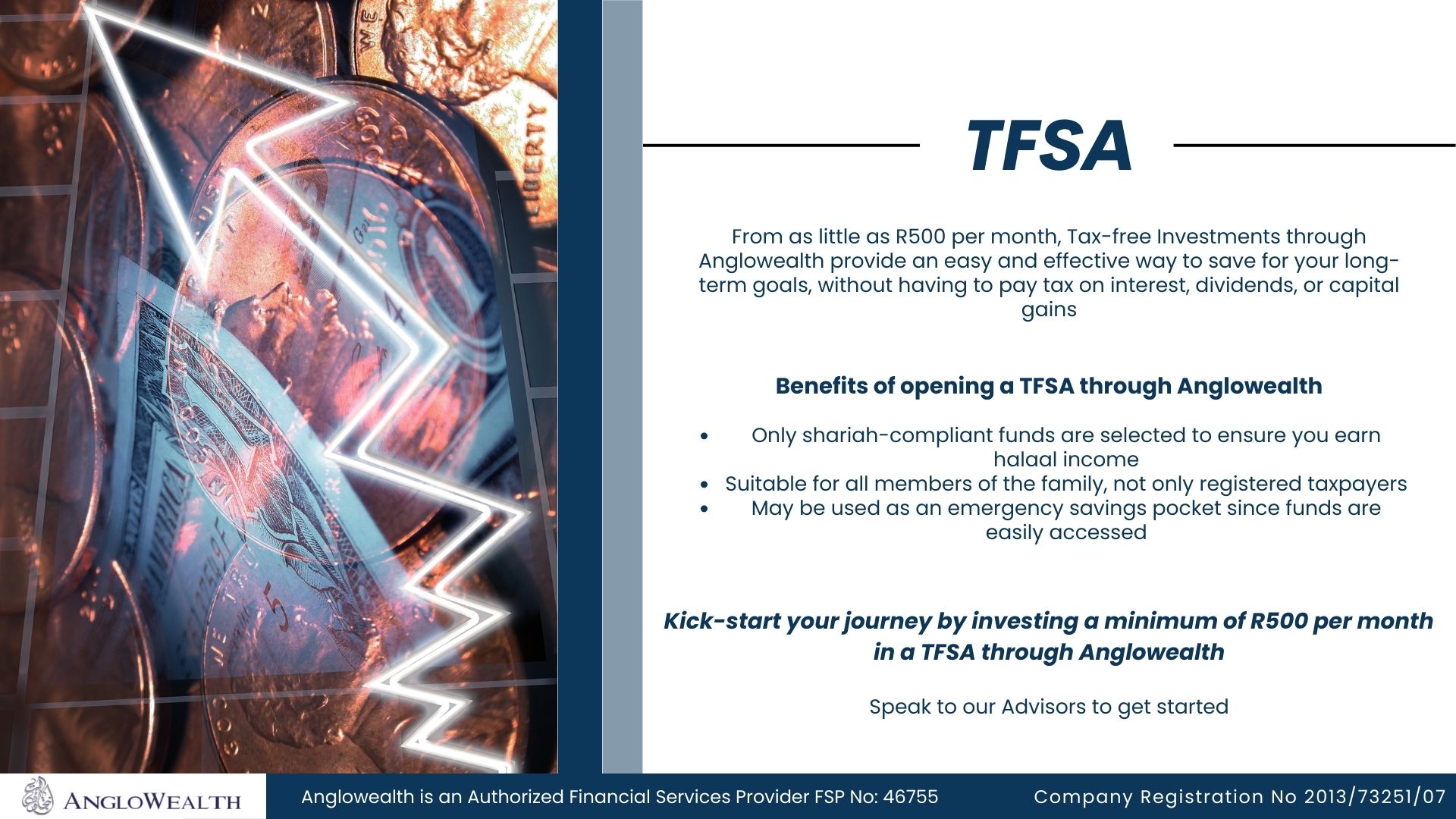

WHAT IS A TAX-FREE SAVINGS ACCOUNT?

Tax Free Savings Accounts are perfect starter investments. Save up to R36 000 per annum, where the growth and income you receive on your investments are totally tax free! No capital gains tax (CGT) or income tax are levied on the dividends and profit received. you can select one or more funds from the various top tier funds we offer.

The fund managers invest your money in a portfolio of assets such as equities, bonds, cash and listed property. The fund is managed according to the fund’s objectives, (such as beating inflation), which determines the return on your investment.

BENEFITS OF INVESTING INTO A TAX FREE SAVINGS ACCOUNT

- As Tax Free Savings Accounts are not subject to income or capital gains tax, they provide a convenient and flexible way to accumulate savings over time;

- Parents can invest on behalf of minors, but withdrawals can only be paid into a bank account in the minor’s name;

- Minimum contribution: Lump sum: R5 000.00 Monthly: R500.00;

- Maximum contribution, R2750 per month, R36 000.00 per tax year, R500 000.00 over your lifetime;

- If you exceed the maximum investment amounts, you will be subject to 40% tax;

- If you withdraw money from an existing TFSA and re-pay it into an of these accounts, it will be regarded as a new contribution and re-use a portion of your tax-free limits;

- There is no limit on your investment term.

A living annuity allows you to invest your retirement savings to generate and draw an appropriate level of income that keeps pace with inflation after you retire.

How do I decide if a Living Annuity is right for me?

Deciding on a product that has to provide you with an income for the rest of your life is one of the most important financial decisions you have to make. If you don’t feel equipped to make this decision unaided, you should consider talking to an independent financial adviser.

An alternative product to consider is a guaranteed life annuity. When making this decision, consider your personal needs, your risk appetite and the key differences between the products available:

-

- In a living annuity, any investment return earned belongs to you and gives you the chance to increase your income over time. In a guaranteed annuity, your income is known in advance, and any additional investment return belongs to the product provider.

- A guaranteed life annuity will provide you with a specified income for a set period of time (usually until you die), while your income from a living annuity, and how long it will last, will depend on the return you earn and how much you choose to withdraw. If you draw too high an income, you may run out of money.

- The company that provides the guaranteed annuity carries all the investment risk. In a living annuity you take the risk that your investment will not perform as you expect, and that you may need to draw a lower income than you would like.

- Living annuities can be left to your beneficiaries when you die but guaranteed annuities cannot be passed on to beneficiaries.

What type of savings can I transfer into my living annuity?

-

- A living annuity is legally restricted to only accept transfers from retirement funds:

- Preservation Funds

- Pension and Provident Funds

- Retirement Annuities

- Other Living Annuities

- You may not add any everyday savings (such as debit orders, lump sums from your bank account or other investments) to your living annuity.

How much income can I withdraw each year from my living annuity?

You can choose how much income to draw, within the legal limits between 2.5% and 17.5% pa. Thereafter, your annual income will automatically revert to what it was before the relief period and must again be between 2.5% and 17.5% pa.

Research has shown that your income has the best chance of lasting until you die if you withdraw a fixed rand amount (rather than a percentage) starting at 4% or less at retirement, and only increase the rand value of your income by inflation each year after that.

When can I change my income level and frequency?

You will only be able to do this once a year, on the anniversary of the date that your living annuity was started.

Can I keep investing into my living annuity?

A living annuity is legally restricted to only accept retirement savings transfers. You cannot continue investing into your living annuity.

How is my living annuity taxed?

The return you earn in a living annuity is not taxed. However, your income is taxed at your marginal income tax rate, depending on the level of income you choose.

We will deduct the necessary tax from your income payment and pay this over to SARS on your behalf.

Reasons a living annuity may not be suitable for you

-

- When your income is not guaranteed as the investment depends on the value and return that you earn. If your investment value drops, or you do not earn enough return, you may need to draw a lower income than you would like.

- If you withdraw too high an income, your investment might not last.

- Investment performance fluctuates over the short to medium term. You take on the risk that your investment will not perform as you expect.

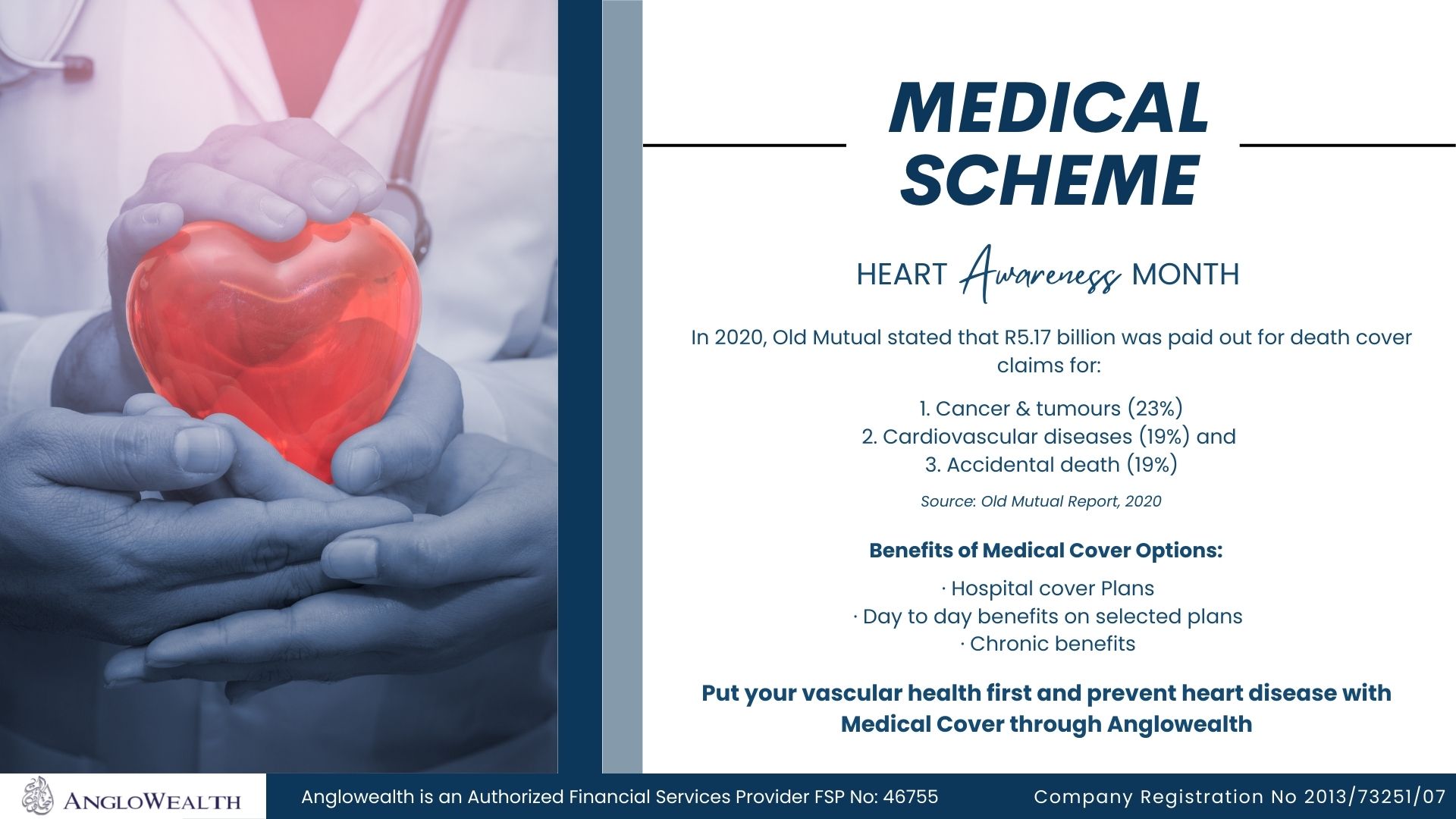

WHAT IS A MEDICAL SCHEME?

Medical Schemes are designed to take care of your healthcare needs and expenses such as the cost of hospitalization, chronic medication, your day-to-day GP visits and emergency care.

We can assist you in selecting the best option of Medical Schemes that suit both your wallet and your healthcare needs.

FEATURES AND BENEFITS

- Through Medical Scheme cover, members can access some of the best private hospitals in the world.

- Medical Schemes pay for many other healthcare needs, such as nursing, surgery, dental work, medicine, physiotherapy and eye-care.

- A Medical Scheme protects members financially in the event of unexpected medical costs.

WHAT IS GAP COVER?

Gap Cover is a medical product that works in conjunction with your existing medical scheme to cover the shortfall of your medical schemes.

In a nutshell, when your Medical Scheme does not pay your private healthcare fees in full, your trusted Gap Cover provider will.

FEATURES AND BENEFITS

- Covers tariff shortfalls of 200-500% over and above normal tariff rates.

- It covers doctors, specialists, in-hospital medical treatments and surgical procedures.

- Upfront fees and co-payment shortfalls are also covered.

- Gap Cover limit per person is up to R160 000.00 per year.

Anglowealth now offers Medical Schemes and Gap Cover.

Discovery Health, Momentum Health, Bonitas, Profmed, African Unity Health, Stratum Benefits, Zest Life, Turnberry, Sanlam.

WHAT IS A UNIT TRUST?

Unit Trusts offer an easy, convenient way to invest. Simply put, a pool of investors’ money is used to invest in financial instruments such as equities (shares) and bonds. This pool is then divided into equal units where each unit contains the same portion of assets in the fund. Investors then share in the fund’s gains, losses, income and expenses. The wide variety of unit trusts means that they are an ideal way to build up a well-diversified investment portfolio tailored to meet your specific needs, risk profile and investment requirements.

FEATURES

Monthly minimum investment: R500.00

Lump-sum minimum investment: R5 000.00

Annual Tax Free limit: R36 000.00

Lifetime Tax Free Limit: R500 000.00

BENEFITS

- You have the flexibility to tailor a portfolio to suit your specific investment needs and time horizon;

- Unit Trusts are tax-efficient, providing tax exemptions on profit income, capital gains tax exemptions;

- Exposure and access to stock market related products allows you to diversify (spread) your investment across markets sectors and economies greatly reduces your investment risk;

- Excellent savings pocket for all ages;

- Funds invested in Unit Trusts is easily accessible, especially in times of emergency;

INTRODUCING THE HAJJ SAVINGS PLAN?

Embark on the sacred pilgrimage to Makkah and Medina, a journey every Muslim dreams of. Anglowealth presents the Hajj Savings Plan, tailored for South African Muslims. Your Gateway to Spiritual Fulfilment

Because we understand your aspirations and have tailored a unique savings fund just for YOU!

FEATURES AND BENEFITS

- Minimum Initial Investment: R 5000

- Hassle-Free Redemptions

- Tailored for South African Muslims

- Flexible Contribution Options

- 14%pa Return

- Investment Term 24months - 18 Years

The AngloWealth Private Wealth Shareholders fixed return capital protector loan agreement, is a five-year, capital-protected investment linked to Shariah compliant Investment principles, that offers the client two non-penalized withdrawal opportunities at selected intervals during the five-year investment term.

How it Works

The full invested capital amount will be allocated to the AngloWealth portfolio as per the allocation model below. Clients have the ability to withdraw 50% of the first year’s profits paid out at the end of year one. A further 50% of profits generated in years two and three will be made available at the end of year three. The combined balance of accumulated profits will be paid out in year five. The investment will yield an annual return of 14% on the capital amount invested. If the client wishes to waive the two withdrawals in year one and three then they will receive a rate of return at 15% in years four and five. The invested Capital amount is secured during the five-year investment term.

Who is it suitable for?

- Want to invest in and have a minimum lump sum of R2 million.

- Are Shareholders who form part of the AngloWealth high valued Shareholders.

- Are looking for a longer investment term.

- Understand and are comfortable with the AngloWealth brand.

- Do not want to risk losing any capital, provided they are committed to the full term of the investment.

- Would like to earn attractive Fixed Returns and at the same time gain access to liquidity at selected intervals during the investment term.

- Would like to diversify their portfolio in AngloWealth.

Investment Details

- Minimum Investment: R2 million

- Duration: The investment is made for 5 years in a fully Shariah compliant investment structure.

- Rate of Return: The investment yields a return of 14% per annum, structured on Shariah principles.

- Capital Guarantee and Growth Exposure Risks: The investors capital is protected and the exposure of the funds in the portfolio is associated with Shariah compliant investment principles.

- Fund Allocation: The funds are invested in our diversified portfolio comprising of Commodities, Property, Oil, High Valued Items, as well as Trade, Asset and Vehicle Finance.

- Tax: The investment returns are before tax. Therefore, Investors are encouraged to obtain their own advice.

AngloWealth Certificates